We all think we know about money. But do we understand the functions of money, what money actually is, and what it represents?

Debt, Trust and the Functions of Money

Public markets were first established less than 3,000 years ago for people to buy and sell using the new invention, money. Market in Kolkata, India. Photo by Bernard Gagnon.

How and when did the first money appear? Do we think of it as a way to measure value? Is it a reliable store of value? Who actually creates the money we use? Is it a commodity to be traded? And how does this money actually relate to our status, to the real value of things we use in our lives, to the effort we make to get them, to the real economy of human settlements?

Once you start thinking about it, these are remarkably slippery questions, questions which have fooled many throughout millennia. Mostly because the answer seems so obvious. Is it not the coin in your pocket, the dollar bill in its clip, the credit card in your wallet, a mobile payment notification on your smartphone, or a cryptocurrency transaction on the blockchain? Money is all these, and none of them, for it is primarily a way of ordering our lives. But this in a particular, arbitrary way: an attempt to make the often indeterminate qualities of our experience fit neatly into quantities; quantities that can be counted and compared to standard units of account, where everything is valued against a sum of money.

“…money is not really a thing at all but a social technology.”

As Felix Martin wrote in Money: The Unauthorized Biography, “The problem is that money is not really a thing at all but a social technology: a set of ideas and practices which organize what we produce and consume, and the way we live together. When it comes to money itself—rather than the tokens that represent it, the account books where people record it, or the buildings such as banks in which people administer it—there is nothing physical to look at…But currency is not itself money…Coins and currency, in other words, are useful tokens to record the underlying system of credit accounts and to implement the underlying process of clearing [these accounts].”

Unfortunately, when we think of money (a noun), we automatically think of coins, of valuable metals, not of an institution by which a process of trust is administered (a verb). We should not think of what money is, but of what money does. For the crucial fact about its nature is that money is a technology, or procedure, devised to manage trust, trust that a creditor will be repaid. One could say it is the operating system on which we run our economies. For to trust is to have a belief in someone, to credit him, and if s|he is obliged to you, s|he is in your debt (hence, credit and debt)—a fact clearly asserted by the Knights of Malta, when in 1565 they stamped this motto on their coins: Non Aes, sed Fides—Not the Metal, but Trust.

But is it always safe to trust those who issue money? They can be defeated and their government can disappear, they can cheat and clip the edges of the coins so that they become lighter and worth less, they can withdraw the currency or let it devalue through inflation. The fact that they are not always trustworthy is one reason why the precious metal in the coins was so often assumed to be the actual thing of value, mistaken for the insubstantial process which the idea of money represents.

The idea of money is one of the most important inventions of settled peoples.

The coins were never the money. They only stand in for the money. They were always tokens. Tokens of trustworthiness, that a debt will be repaid. And tokens are only tokens, however rare and valuable the metal they contain.

Despite all its ambiguous attributes, its dependence on confidence and trust, and the ease with which it can be used to cheat, the idea of money is one of the most important inventions of settled peoples. For it is one of the key technologies that allowed much larger groups to thrive together than was possible before. But like all technologies, it is a two-edged sword which can be used to steal as well as pay.

The Rai of Yap—a Very Odd Kind of “Money”

A large (approximately 8 feet in height) example of Yapese stone money (Rai) in the village of Gachpar. Photo by Eric Guinther.

When Westerners first came upon the remote island of Yap (Federated States of Micronesia) in the 19th century, far from anywhere in the Pacific, they were surprised to find that the islanders used a bizarre currency. It consisted of large circular discs of limestone with a hole in the middle. These disks, called Rai, were between 1 and 12 feet in diameter. They were quarried from an island called Palau, some 280 miles away, and carried from there by outrigger canoes, to be propped up around the island, and part-owned by one person after another, representing value. Some were even shipwrecked at sea, but remained as part of the currency, for everyone knew their quality, history, position, value and current owner.

These stone disks could in no way be carried about and used as coins, but they were currency, for they were assigned in payment for specific social exchanges: marriages, inheritances, political deals, even pigs. More mundane items, like food and fibers, could be exchanged for shell money, or through a customary obligation in which it was obvious who owed how much to whom, and repayment was expected to occur in kind, when the time came.

If one looks up the Rai, it is simply called money. In one sense this is true. But it is also profoundly misleading, for a Rai is not a currency which can buy you anything and everything, it is only a marker or token recording the value of a changed relationship which has been entered into by two parties, in certain circumstances—a kind of contract.

It indicates the existence of a particular social linkage, in that particular society. It is one of the means whereby social relations are ordered, whether they are relations involving power, family connections, transmission of status goods, or family obligation. In Yap, the monetary system relies on an oral history of ownership. Each transaction is recorded in this history, and no physical movement of the stone is needed; no physical possession, as with metal coins.

Reciprocity and Obligation in Non-commercial Cultures

Indeed, for most of human existence as hunter-gatherers, interchange was governed by social reciprocity; obligation to be helpful, fair and just according to tradition. To be fair to other members of the family, of the village, of the tribe. To participate in the essential sharing of effort and goods which maintain the community. To behave in accordance with the rules of rank and status. The kind of sharing which occurs in families, where repayment is not expected.

There was no universal, abstract, measure of value; no actual money. For there was no commerce as we know it, no established market in which goods could be traded. It was social obligation and status which held societies together. In these small societies it was easy and natural to keep track of who was pulling his weight and who was not. Daily transfer of necessities was done by an informal system of reciprocity, in which a notional unit of exchange was never needed.

Example of an ornamental copper used at a potlatch.

In more complex societies, reciprocity was formalized through the giving of gifts. Serial exchange of gifts established alliances, created obligations and denoted solidarity. In certain societies giving became an almost aggressive act, as in the competitive distribution or utter destruction of wealth by high-status individuals asserting their hierarchical position in the potlatch ceremonies of the indigenous people of North West Canada; ceremonies in which the host challenged a guest chieftain to exceed him in his ability or “power” to give away or to destroy goods, valuable items, like blankets or ornamental copper shields (worth the same as a slave). British colonizers considered such practices primitively wasteful, and contrary to the “civilized values” of accumulation, and tried to suppress them. But such profligacy is essential to the maintenance of the very structure of that society. Something considered more important than the hoarding of mere goods, or the colonizers’ money.

To modern Westerners, the customs of other peoples often look bizarre when compared to our commercial practices. Commercial practices that give us access to status goods like fancy clothes, or necessities like bread, and for which we pay with money.

Raffia cloth from Angola ca 1866. Cloth mats like this were used to make payments by many of the peoples of Angola and the Democratic Republic of Congo.

For instance, the Lele people of central Africa, in what was the Belgian Congo, with whom the British anthropologist Mary Douglas lived in the 1950s, did have a sort of currency, a piece of raffia cloth; cloth which a man could weave in about three hours.

But these cloths were not used as a currency to buy daily goods. Instead this “cloth money” was restricted to a particular variety of non-commercial “payments” which were required in Lele society, and for which “cloth money” was needed. Their function was to maintain social relationships within the Lele. Cloths were used as entrance fees to religious cult groups, fees to ritual healers, for marriage dues, as a reward to a Lele wife for giving birth, as fines for adultery, as compensation for fighting and blood debts, and as tribute to chiefs.

The Lele valued raffia cloth as highly as Europeans valued gold. But because the structure and values of Lele society were very different, payment in cloth was made in very different circumstances. The motives for payment were social, not commercial.

This system meant that older men owned more cloths than the younger ones. They were richer and had more power; power to control the younger men, who had to borrow from them in order to join the required cult groups, or to marry. However, as contact with Westerners increased, cloths were traded for Belgian money, and an exchange rate between them established. A young man could work for the foreigners and, with his pay in franks, could buy cloths to bypass his elders and, for instance, use the cloths to join a cult group. So the traditional structure of social control across the generations was progressively weakened and the society disrupted by this contact with an alien system of money.

Societies with extremes of riches were linked with power and conquest, with tribute, plunder and booty. Rule was always linked with access to riches, but not to trade, and seldom have traders been granted the status that businessmen have now.

This shell money, called diwara, is from the Duke of York Islands in East New Britain Province, Papua New Guinea. It features a series of Nassarius shells, threaded on to pieces of cane. Queensland Museum.

Where there was trade, mutually agreed values were used, equivalent to a kind of monetary standard. This money could be represented by a certain weight of silver, by a rare shell, or even by an iron meat-skewer, an obol, as in pre-classical Greece. Always an intermediary substance was used which could be valued as a standard in relation to the commodities being traded. A cowrie shell could be worth two yams, or one sea cucumber. But barter was always rare and only used in extreme situations. No modern archeologist or anthropologist has ever found a society which regularly made its trades through barter.

Proto-accounting: Correspondence Counting

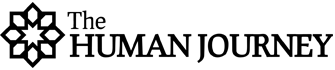

Small baked clay tokens used for keeping records by correspondence counting.

In Mesopotamia, archeologists found quantities of curious little clay objects: cubes, pyramids, cylinders, cones, some of them 8,000 years old. At first these seemed like gaming pieces for something like chess. But no gaming boards were found. Finally, in the 1970s, the French archeologist Denise Schmandt-Besserat realized that each shape actually represented a different commodity in daily life: a sheep, a loaf of bread, a jar of honey.

Such counters were adequate to record small transactions. A few items at a time could easily be kept as a record of a transaction; clay counters used for primitive accounting; for correspondence counting, as it is called. Correspondence counting is easy: you don’t need to know how to count, you just need to look at two quantities and verify that they are the same. These little clay objects were tokens of proto-money.

The Challenge for Centralized States

By 5,000 years ago (3000 BCE) centralized states were established in the Fertile Crescent, states run on bureaucratic lines, with hierarchically controlled command economies, where goods were rationed. Military dictatorships of a kind. Their size and complexity posed quite new and difficult problems of organization. For an urban economy needs planning and taxation. It needs to feed its troops, and there is trading too. These states were centered in cities, such as Uruk, in Mesopotamia, modern day Iraq, on the banks of the Tigris, with a population of over 50,000.

Map of the Middle East during the last centuries of the 4th millennium BCE: archaeological sites of the “Urukean expansion.”

Here the specialization of civic and technical roles for different people first occurred. There were farmers, and craftsmen, and soldiers, all organized under a bureaucracy of priests, ruled by a priestly monarch. Each had a part to play.

The way these states were organized involved the collection and re-allocation of all goods to and from central storehouses. These were managed by the ruler’s priestly bureaucrats, to whom the farmers brought their produce from the fields around the city. This produce was then consumed by the rulers, by their non-productive soldiers, by the priestly administrators, by the productive artisans who made the tools, the arms and ornaments, by the traders and by the farmers themselves. This system served all needs, even in time of famine.

Imagine the world’s first accountants, sitting at the door of the temple-storehouse, using the little tokens to count as the stores arrive and leave; so much grain, oil, dried fish. This would become a very laborious business. So how to keep track of all this coming and going?

The Invention of Accounting, Writing and Numeracy

The answer was three momentous inventions: accounting, writing and numeracy.

(1) Accounting, which could manage tokens representing large quantities and divide them into portions, and relate these to use, over time.

(2) Writing, which made a permanent record of the accounting.

Globular envelope with a cluster of accounting tokens. Clay, Uruk period (4000 BCE–3100 BCE). Louvre Museum.

(3) Numeracy, which created a new concept—number—a concept that could represent quantity without having to count actual tokens.

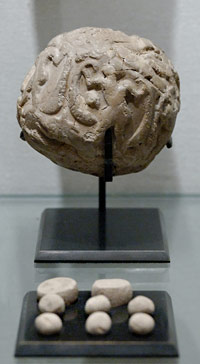

Accounting began when a number of clay tokens were first inserted into a clay envelope. The envelope was sealed and tally marks were made on the outside to denote the kind and the number of tokens inside; five sheep, ten baskets of grain, seven jars of honey.

The marks were used to record the back-and-forth of the tokens, which themselves were recording the back-and-forth of the sheep, the grain, and the jars of honey. But something revolutionary had happened. The abstract marks on the envelope-tablets matched the tokens inside which were no longer counted, but were read off from the surface of the envelope. It may be that the first such envelope-tablets showed impressions of the tokens themselves, pressing the hard clay tokens into the soft clay tablet.

Clay accounting tablet from Uruk. Impressions represent numerals and commodities. Pergamon Museum in Berlin.

Soon the ancient accountants realized it would be simpler to make the marks not with the clumsy tokens, but with a reed pen; to supersede three-dimensional objects with two-dimensional symbols. Thus cuneiform writing was born, composed of lines, of triangles, circles and other marks. A stylized picture, representing an impression of a token, representing a commodity.

Early writing on an economic tablet with numeric signs. Proto-Elamite script in clay, Susa, Uruk period (3200 BCE to 2700 BCE). Louvre Museum.

Then, in a further burst of creativity, they began to use different marks for (1) a commodity and (2) its quantity. Now only two symbols were needed to record any quantity of anything (even the 140,000 measures of grain, which appear on one tablet). This separation was a double invention, of (a) symbolic writing and (b) numeracy. The writing down of numbers, made things much clearer, and the process of recording exploded. Vast numbers of tablets have been found in Mesopotamia, records of money transactions and contracts, dating back to more than 5,000 years ago.

So out of the process of recording quantities of concrete objects, writing appeared. Writing which could then be used to record our thoughts on other topics, to write down stories and to crystalize ideas. A technology invented to transmit our thoughts across both space and time.

Primitive Money—with Multiple Denominators of Value

But there was still no actual money, no abstract idea to represent value, and no coinage. There was only accounting (and auditing; the hearing of the accounts as they were read out). Mostly there was no need for a unit of account, as it was the actual commodities that were being accounted for: the baskets of grain, the sheep, the jars of honey. There was little trade between individuals, no market. What was essential was that the authorities keep track of what was where, and when, and that what was planned had been accomplished, or not. (Much as happened in the command economy of the Soviet Union later on.)

But, as elsewhere, there was trade. Timber, precious metal, slaves, and perfume from abroad were traded for the local cloth, pottery and other artifacts. And where there is trade, a money of account is needed; a money based on measurement, on metrication, on commonly agreed units of weight. For instance, a certain weight of silver would be equivalent in value to a certain amount of timber, and a different weight of silver would be worth a basket of barley. The most commonly used denominators of value were weights of silver, copper, tin, lead and barley. These weights even had names, such as Shekel, Mina and Talent, with 60 Shekels to a Mina, and 60 Minas to a Talent. But these were not units of money, only of weight of silver.

Money as a Universal Scale of Economic Value—The First Coins

The momentous invention of money, as both a universal, and a decentralized, scale of economic value, only occurred long after the invention of accounting, and it probably occurred in tandem with the invention of standardized metal tokens—coins. With them, came markets, too.

As Felix Martin writes:

This spread of money’s first two components—the idea of a universally applicable unit of value and the practice of keeping accounts in it—reinforced the development of the third: the principle of decentralized negotiability. The new idea of universal economic value…

Now money was opening up a still more radical horizon: traditional social obligations could not only be valued on a universal scale, but transferred from one person to another. The miracle of money had an equally miraculous twin—the miracle of the market. And with the invention of coinage, a dream technology for recording and transferring monetary obligations from one person to another was born…

Markets require people to be able to negotiate a sale or agree a wage on their own, instead of feeding their preferences into a central authority in order to receive back a directive on how to act. But successful negotiation requires a common language—a shared idea of what words mean. For markets to function there therefore needs to be a shared concept of value and standardized units in which to measure it. Not a shared idea of what particular goods or services are worth—that is where the haggling comes in—but a shared unit of economic value so that the haggling can take place at all. Without general agreement on what a dollar is, we could no more haggle in the marketplace over prices in dollars than we can talk to the birds and the bees….

A 640 BCE one-third stater electrum coin from Lydia. Photo from Classical Numismatic Group.

It was not until sometime in the 7th century BCE, two and a half millennia after the Uruk period, that the first metal coins appeared. They were minted in Lydia (what is now Western Turkey), and were made of electrum, a natural alloy of gold and silver. This invention was soon copied by other Greeks around the Aegean Sea. By 480 BCE there were nearly one hundred mints in the region.

Coins were a great improvement on previous units of account. They were small and valuable, and above all, they could be standardized in value. So perhaps ten coins could buy a horse and twenty buy a slave. What’s more, no weighing was needed to transact a deal, and better still for some, the process was anonymous.

Everywhere, traditional social obligations were transformed into financial relationships. In Athens, traditional agricultural sharecroppers were converted into contractual tenants paying money rents. The so-called ‘liturgies’—the ancient, civic obligations of the thousand wealthiest inhabitants of the city to provide public services ranging from choruses for the theatre to ships for the navy—were now assessed in financial terms…the rewards granted by the state to victors at the Pan-Hellenic athletic competitions began to be prescribed in monetary terms…500 drachmas for a champion at the Olympics…

By the fifth century BCE Athens was, in the words of the great politician Pericles, ‘a salary-drawing city’. Jury, magistracy, and military service were all paid in money. Citizens were paid to attend public festivals and even, by the fourth century BCE, to turn up to the assembly to vote on legislation.

But coins were not used for every occasion of trade, for they were relatively scarce, and relatively high in value. So most items were still only traded on credit, people kept account of what they sold and what they were owed. The coins were minted to collect taxation. Taxation paid for administration, city monuments, and war. It was the citizen army, and the mercenaries, who were paid in coin.

Nevertheless, the Greeks, despite their speedy adoption of metal coinage, treated it with suspicion. For they saw that the exchange of metal coins for goods, services, or loans did not always represent the exchange of actual organic wealth.

To illustrate this, and warn against the error of avarice, the Greeks told the story of the mythical King Midas, who, it was said, asked the gods to grant him the ability to turn everything he touched to gold. The gods agreed, but this was a disaster. For nothing was spared from the gods’ decree. Everything he touched turned to gold. When he touched his daughter, she was turned to gold, and reaching for his food, it turned to lifeless gold. And so, childless, he starved. A cautionary tale, if ever there was one.

Money Tokens Elsewhere

Seleucid (Greek) coin from India. Obverse: the head of Zeus, Reverse: Athena with elephants. Photo from the Classical Numismatic Group.

Coins soon spread around the whole Mediterranean, and the Greek idea of coinage traveled as far as India with the conquests of Alexander the Great (356–323 BCE), though some Indian coins have been dated a little earlier, to about 400 BCE.

Every major civilization has invented its own kind of tokens representing money. For instance, the Chinese issued bronze spade money-tokens about 600 BCE and sword money-tokens at about 450 BCE. They also used round bronze coins, with a hole in the middle. Later on, in the 10th century CE, the Chinese used printed notes on paper made from bark, fiat money, not backed by anything of value.

Chinese spade money (ca 650–400 BCE), coins (ca 7 CE), and paper money (ca 1287 CE).

Even wood was used as money. In England around 1,100 CE, King Henry I, during one of the recurrent gold shortages of the Middle Ages, began using tally sticks as money, with which his subjects could pay taxes. Squared hazelwood tallies were most common, about eight inches long. These were notched to indicate the amount paid, and then split so that the notches appeared on both pieces, called the stock and the foil. The stock was held by the king as tax money, the foil by the subject as a receipt.

Medieval English split tally stick (front and reverse view). The stick is notched and inscribed to record a debt owed to the rural dean of Preston Candover, Hampshire.

When tallies were used to register loans to King John around 1200 CE, the result was that the money lent was, in effect, doubled. For the king could spend the value of the stock, the half he held, and his subject, who held a foil of the same value, could also trade his foil for other goods. Such tallies were used till 1826.

The Janus Face of Money

A bronze Roman coin from Canusium depicting a laureate Janus (209–208 BCE or later). Photo from Classical Numismatic Group.

Money has always been two-faced, appearing both as a technology, and as an object of value. It began as a process of accounting, by relating the value of many different things to a standard one; to the value of a weight of silver, or a bushel of grain. It later developed into something more abstract, not related to a commodity, but to a universal scale of economic value. However, because people find it easier to think of objects than to think of processes, they focus on the object, the piece of silver, and ignore the process which defines the meaning of the idea. They mistakenly think of the value of money, rather than valuation by money.

They mistakenly think of the value of money, rather than valuation by money.

Confusion was compounded with the invention of coins in the 7th century BCE. Coins are made from precious metal for very good reasons. Gold and silver are rare and therefore valuable. They are also stable and dense. Their density allows them to be small and portable, unlike the stone disks of Rai. They are also malleable, so can be stamped with images, making it easy to distinguish them.

So, when the idea about the measuring unit of value, money, was turned into something actually valuable, into gold coins, they seemed to be the actual commodity, rather that an intermediate measuring device. Since then, this mistaken idea, that the token for money, the coin, is the actual wealth, has caused much confusion about the nature of real wealth. A confusion at the root of many crises, and a plague on our philosophers, economists, and politicians.

Before coinage there had been systems of accounting for wealth and for debt, and it was quite clear what was going on—there were so many cows, or so many bushels of barley, and one person owned so much, or was in debt for so much to another. It was easy to understand what constituted wealth: it was the strength, skill and knowledge of that society, the land and goods which it controlled.

But coins, once they were invented, were no longer just measuring devices, tokens. They assumed the Janus face of wealth itself. The intrinsic value of the precious metal in them focused everyone’s attention on the tokens. The tokens became the items for which to strive, and blinded us to the real meaning of money, which, in the end, measures and transmits the power that we have over our environment and each other.

This confusion still persists today. Money tokens, even electronic ones, are seen as actual wealth, even when precious metals no longer figure in our money systems. They continue goading us with ever more desire in the commercial dreamworld that we now inhabit. A dreamworld in which debt is misinterpreted as actual wealth, and qualities which do not fit into the realm of property, qualities like care, air purity, or health, are measured, inappropriately, by money, in a vain attempt to make them interchangeable with property. For what is money in our time, but an illusory idea of universal value, a process that aims to reduce all items, acts and qualities down to a single mode of valuation. So long as only a small minority understand all this, the rest of us are open to both moral and financial exploitation.